Time flies! At the time of writing it’s been 1 year, 2 months, and 11 days since I separated from my last employer. On my own to support my lifestyle solely through my investment portfolio – so what did I learn during this time being Financially Independent? This is just a quick post that’ll hopefully help you in your journey.

Lesson 1: Inflation Proof Yourself!

I mentioned this in a previous post but the fewer expense line items we carry in our budgets the less inflation will affects us. If you’ve seen the movie Fight Club there’s a quote that resonates here:

The things you own end up owning you.

Tyler Durden

For instance, if you have 2 cars. They’re both subject to inflationary pressures. The hourly rate for maintenance/repair is subject to inflation, insurance is subject to inflation, replacement parts are subject to inflation, and the gas or electricity used to power the vehicle is subject to inflation as well.

You can reduce your overall exposure to inflation by reducing the number of ‘things’ you own. If you can halve the number of expense items in your income statement you can shield yourself from the inflation. So do consider the amount of ‘things’ you own.

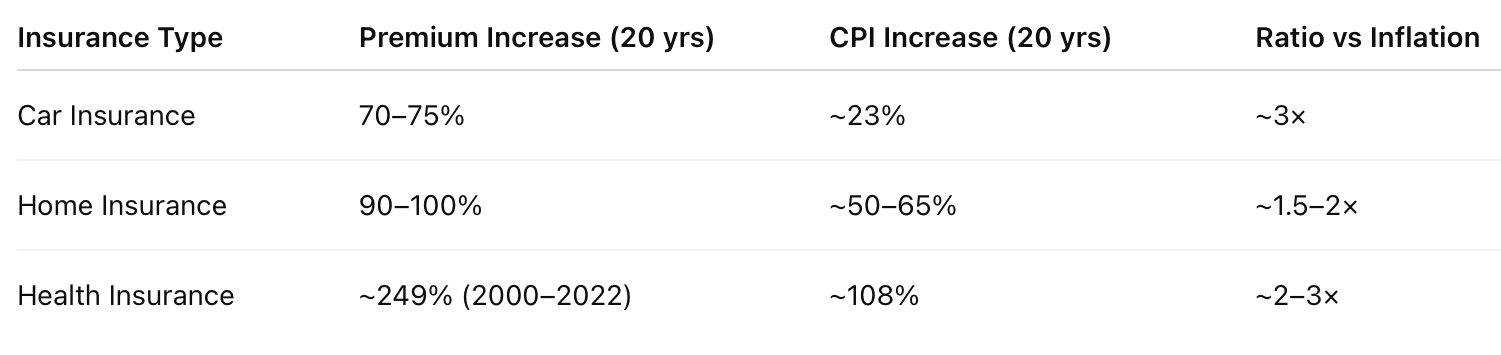

Lesson 2: Insurance is Really Expensive

The cost of insurance generally outpaces the rate of inflation. This includes home insurance, car insurance, and if you live in a country without universal healthcare, like the United States, health insurance too. This is largely due to the increasing occurrences of climate disaster, auto theft, vandalism, and increasing cost of healthcare. Here’s a snapshot of how these three categories of insurance have outpaced inflation over the past 20 years:

While we can decrease the number of ‘things’ we own that need to be insured, we can’t entirely eliminate them. When forecasting budgets prior to retiring make sure you account for a separate rate of inflation for insurance using historical data and put money aside to address year over year rising costs.

Lesson 3: Dreaded Items on the To-Do List

When you retire you may think you’ll get around to all the things on your To-Do list having all the time in the world….Surprise! You won’t 🙂 You’ll find there are items that even with unlimited amounts of time you’ll lack the desire and motivation to get them done.

I suffer this on the daily. That tub that needs to be re-caulked, the closet that needs to be cleaned out, etc. Still haven’t gotten done and they won’t likely get done until there’s an extrinsic motivator. Such as if I were to sell the home I’d want to maximize profit potential and that tub would get the best caulking ever!

In retirement don’t expect to suddenly feel the urge to do something you never wanted to do in the first place despite having time. Often we make the excuse of not doing something because we don’t have the time when in reality it’s because we just lack the motivation. And that’s ok, you’ll get around to it.

Lesson 4: Stepping Away is Difficult

Quitting a job is one thing, but quitting a career hits on an entirely different level.

The initial feelings of freedom, elation and relief from the pressures and stresses of work are short lived. Perhaps this is just part of the healing process of burnout but after year or so feelings begin to complicate. The employment gap widens and with it come feelings of skill atrophy, self-doubt, imposter syndrome, and perceived future employer biases if you wanted to rejoin the rat race. It’s not easy and these negative feelings can get compounded by a weak job market – if you do endeavor into looking for employment, limited openings/prospects, and receiving rejection after rejection can trigger an unhealthy thought pattern.

If you fall into this camp stay positive and stay connected to your past work if you choose to. Consider using all the unique skills and experiences you’ve gained over your career to help others through freelancing, consultation work, or just mentorship of those following in the same career path. There are so many outlets to do so from LinkedIn to UpWork. Or if you want to re-join a company, not necessarily to work for money but to work for self fulfillment that’s an option as well. Just remember that you and your skill set are valuable despite what a weak market may try to get you to believe.

As for myself – I’m self declared Financially Independent, but haven’t quite accepted Early Retirement just yet 🙂

Lesson 5: FORO?

The Fear Of Running Out of money is real. Going from a high savings, high investment mindset to one of consumption is not easy. To get to the point of Financial Independence you’re likely to have stashed away and invested a large percentage of your income. Once you’re Financially Independent and living off your investments, your investment rate shrinks drastically to meager levels in comparison and it just doesn’t feel right. Withdrawals from the portfolio to fund consumption rubs more salt into the wound leading to doubts and feelings of running out of cash. This is completely normal.

By the way, just as an aside I’m a proponent of early retirees in their 20s, 30s, and 40s to continue to invest or adjust their withdrawal rates well below 4% to ensure a sustainable nest egg. Those retiring in their 50s have lower risk and further investment may not be necessary.

Now back on topic….Anecdotally, I’ve read that the first year of retirement is the hardest but by year two there’s confidence that finances are ok and the money won’t run out. I haven’t hit year two just yet but according to the wisdom of those that forged the path before, there is hope and light at the end of the tunnel. Just stay the course, spend within your allotted budget, and things will find a way to work themselves out.

Before You Go…

Look out for my next post: 5 Wonderful things about Retiring Early. And of course a word from our sponsor! Oh – Still no sponsors 🙁 But I do have an affiliate link for you to help me grow this blog. Here’s WealthFluent in their own words:

WealthFluent: The personalized financial decision-making engine

Navigating changing circumstances and countless variables can make financial decisions feel overwhelming. WealthFluent simplifies the process, empowering users to make confident decisions tailored to their unique financial situation, lifetime goals, and current market conditions.

Our platform provides the clarity users need to:

- Plan for retirement while balancing today’s priorities with tomorrow’s aspirations.

- Understand tradeoffs like risk versus expected return and optimize their financial strategy.

- Adapt financial decisions in real-time as life and markets change.

WealthFluent empowers a more innovative, personalized approach to financial decision-making, helping people align every decision with their long-term vision.

WealthFluent stands for clear and confident financial decision-making.