Just a quick post to double click on Rates of Returns before we get into Asset Allocations.

As individuals we can invest our excess income inflows into real estate, stocks, ETFs, bonds, art, and other asset classes, but the main objective is to be committed and consistent with our investments to allow the power of compounding to grow our wealth over time.

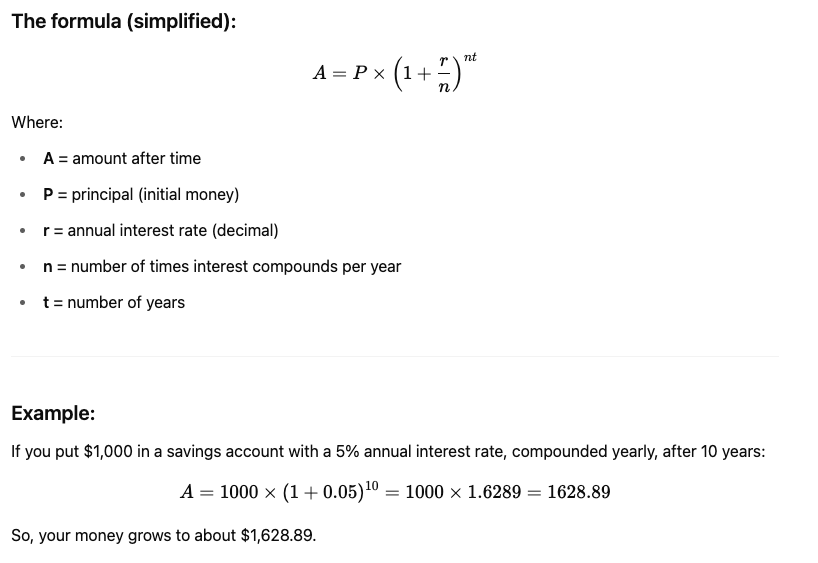

For a refresher on the power of Compound Interest please refer back to my previous post: Run Personal Finances like a Business. Compound Interest can be calculated with the formula below.

Rates of Return

Each asset class and investment provides a rate of return, or “annual interest rate” as represented by the variable ‘r’ in our Compound Interest formula above.

So in theory if we double the rate of return we’ll reduce the time to reach our FIRE ‘number’ exponentially. Go ahead, try for yourself with the simplified compound interest calculator below (it compounds annually).

Note, some asset classes offer negative rates of return! As a general rule, the higher the rate of return the faster our wealth will grow, but with greater downside risk and the possibility of negative returns or even total losses. Also note, past rates of returns are no guarantee for future returns.

Simplified Compound Interest Calculator

Compound Interest Calculator

As you experiment with the calculator don’t get too carried away and focused on chasing the highest rates of returns. We should aim for nothing less than long term profits and growth with our investment strategy. Much like successful businesses around the world achieve. Jeff Bezos founder of Amazon was once quoted:

I don’t believe in bet-the-company bets. That’s when you’re desperate.

Jeff Bezos

Risk and Reward

Let’s quickly highlight two examples. Short term treasury bonds or money market funds offer low rates of return but pretty much guarantees preservation of capital. Over the past 20 years they’ve returned somewhere in the neighbourhood of 2.5%-3% per annum. Where as a simple S&P500 index fund has returned an average of 9.8% per year over the same time period but with many more fluctuations, and higher volatility over that time. Some years were down, some years were up but the general trend over time has been up.

If Sally invested $10,000 into short term treasuries returning 3% annually 20 years ago and Susan invested $10,000 into an ETF tracking the SP500 returning 9.8% annually 20 years ago. Today, Sally would have $18,061.11 and Susan would have $63,870.43.

So Sally who took nearly zero risk of losing her Initial Principal earned $45,809.32 less dollars than Susan over the same time period. Who would you rather be in this scenario? And how do we find a good balance between risk and returns? The answer: Asset Allocation, balancing returns and risk.

Asset Allocation

There’s no need to be restricted to 100% in one asset class unless you have very specific goals and short term cash needs. We’ll cover asset allocation in greater depth in a future posts but the take away for now is that you should run your personal finances for profit, as successful companies do. Invest and grow your nest egg over time with the power of compounding. As opposed to chasing the highest rates of returns which may put you in a disadvantaged position in the long term. The tortoise usually wins the race.

Warning: As stated in an earlier post there are more getting poor fast schemes than there are getting rich fast schemes! Avoid them, take a patient and consistent approach and wealth will build over time.

Less is More

Before you go!

Animal companions are one of the most special relationships we build over our lifetimes and we all want to best for our pets. Health and nutrition are pillars to a long life, what we feed our furry animals matters. Have a look into our affiliate ZEAL PET who manufactures 100% natural, New Zealand-made pet food crafted with love, care, and nutrition in mind. Check out their offerings for Cats and Dogs.

Cat:

Dog: